....AS AN APPENDIX TO MY INFORMATIONAL SUPPLEMENT IN ANSWER TO THE ABOVE CAPTIONED MATTERS, SUBMITTED BY DEFENDANT DANIEL M ROSENBLUM ("I", "ROSENBLUM" and "DMR" below.)

___________________________________

1. This instant filing is NY State Supreme Court, Suffolk County Index # 061458/2013 Efiled Document #16, {DMR#10} Appendix 8 of 18 to DMRAMEX091313, first reference in ¶ 12 and discussed in same DMRAMEX091513 various ¶s including ¶ 20-22 below & ¶,& ¶ 35. "21st Century Digital Analysis/Critique Generally": RE: PERMISSIBLE ACTITIES & TYING IN BANKING INDUSTRY; DURBIN AMENDMENT TO DODD FRANK ACT, 21ST CENTURY DIGITAL, Efiled Document #16

2. This page will be further developed, but, for now must be at a minimum served on the parties and the court as absolutely imperative facet to my September 15 filing and relationship to any debt I have incurred, financial profile DMR in general, and any claim I have regarding counter claims against attorney firms in this suit while action(s) remain open, and also any other 21st Century Digital related actions.

3. Rosenblum is certainly of the opinions that all debts must be repaid. Debt must be repaid. Loans must be repaid. The borrower has a contractual obligation to the lender.

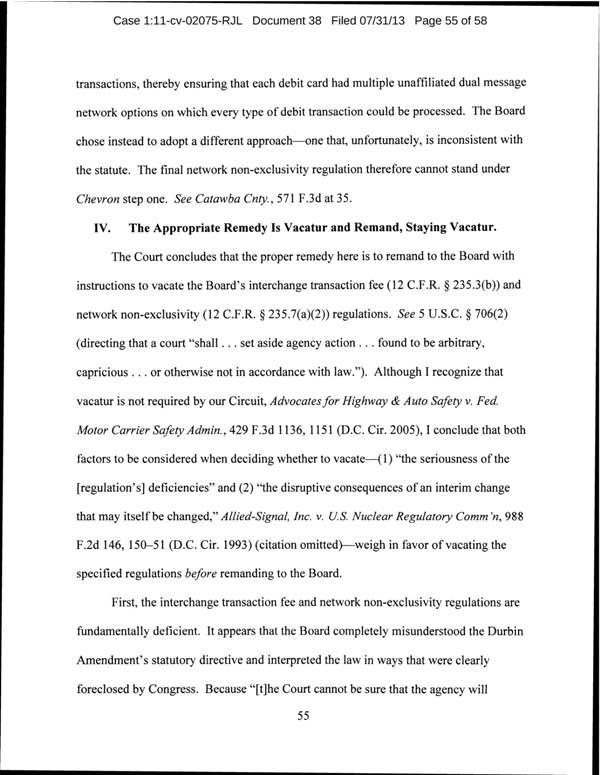

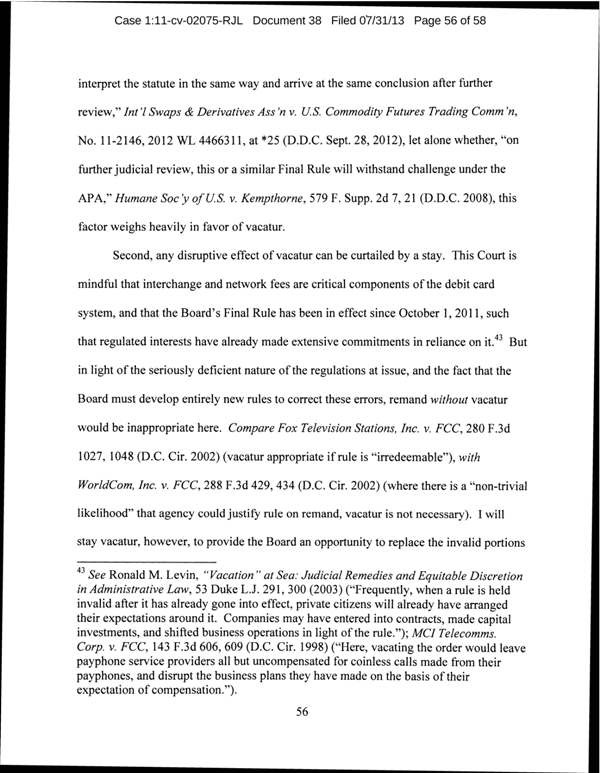

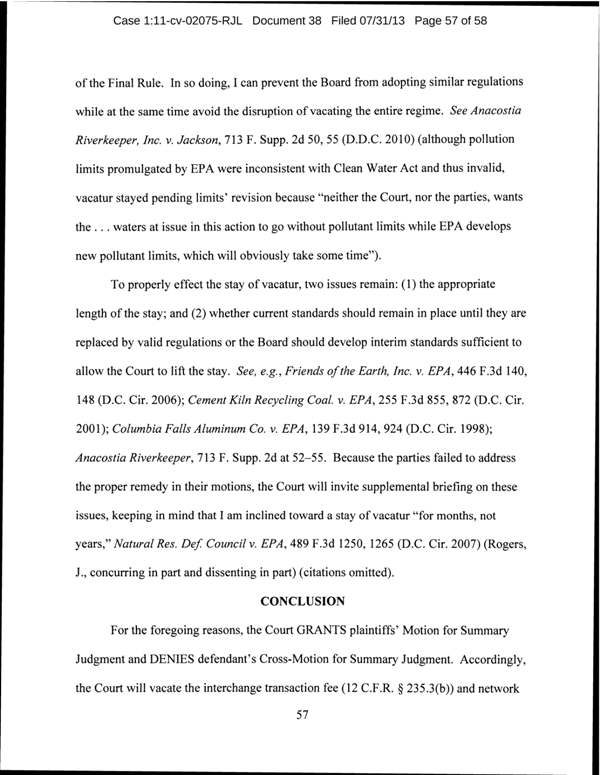

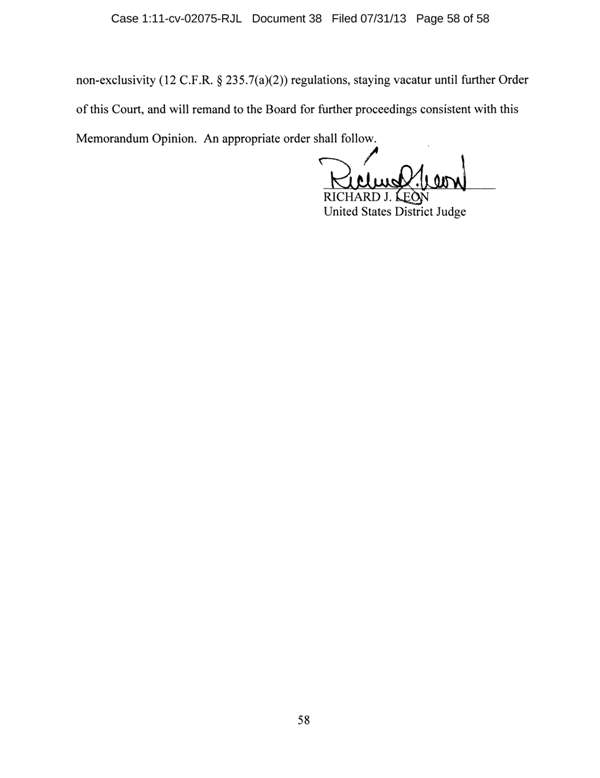

Below, §§¶¶ "Q" of this webpage which carries the full July 31st 2013 decision by Judge Richard Leon in the matter of NACS v. Board of Governors of the Federal Reserve System, 11-cv-02075, U.S. District Court, District of Columbia (Washington). The decision is concerned with debit card interchange fees or "swipe fees" charged by Visa and Mastercard for processing transactions using digital technologies.

Before the images below of the NACS v Board case, there are remarks by Daniel M. Rosenblum, many of the several paragraphs exerpted and edited from Rosenblum's prosecution of his patent application for a 21st Century Digital Network. There are also references to my Main filing of September 15 2013- DMRAMEX091313- the subject matter on this page will be further refined for publication as resources permit:

5. This filing underscores Rosenblum's understanding of the importance of both the Permissable Activities Axiom & the Tying Axiom for the banking industry in a capital economy as a driving force for production, innovation, and efficiency in a capital economy. Rosenblum is a stauch advocate of entreprenuerial endeavor, entrepreneurial endeavor and innovation go hand in hand in a capital marketplace; and Rosenblum is Sole Proprietor of 21st Century Digital, which Rosenblum establised on December 9, 1996, by filing a DBA with the NY County Clerk's at 60 Centre Street NY NY. Please see concluding paragraph ¶ 33 below, for a link and Efile reference to the final Appendix #18 of 18, "Business Certificates: Daniel M. Rosenblum Sole Proprietor of 21st Century Digital, TTS Industries, and TMTP USA Unlimited." Appendix 18 of 18, Efiled Document #27.

As Such.....Rosenblum references here...{for further development and for necessary present deliberation in the current matter}...in this Section Paragraph 5 of Appendix 8 of 18 "21stCentury Digital Critique Generally"...

- "With regards to this Section Paragraph 20, and in continuation of Paragraph 12 above which introduced Appendix 8 Labor Day 2013 E-filed Document #16 regarding the Dodd Frank Durbin Ammendment litigation NACS v Board, for each of my Paragraph 20 Series Appendices below:, the materials are directly relevant to todays filings, specifically insofar as DMR has referred in this filing to a "21st Century Digital Analysis and Critique" as it relates to Banking entities presumably primarily engaged adn deriving revenues and taking advantage of certain aspects of the regulatory landscape available to commercial entities, namely banking entities, engaged in the commercial service of loans, discounts, deposits, and trusts in the US Marketplace all the while also engaged in the commercial service of processing data in the US marketplace which has an annual revenue stream of upwards of 68 billion, in light of two important regulatory doctrines in banking: 1) permissible activities and 2) tying limitations."

Images of the full 59 page decision in NACS v. Board of Governors of the Federal Reserve System, 11-cv-02075, U.S. District Court, District of Columbia (Washington) will follow at §§¶¶ 40 the foregoing §§¶¶ 20 DMR remarks regarding this section 21st Century Digital Banking Analysis /Critique, the writing is mainly culled and edited from DMR Patent , Permissible Activities, and Tying analyses cited above in paragraphs 10-20:

§§¶¶ 20 DMR remarks regarding this section 21st Century Digital Banking Analysis /Critique in approximately 35 numbered paragraphs

§§¶¶ 20, ¶¶ 1-40

DMR remarks regarding this section from DMR Patent , Permissible Activities, and Tying analysis:

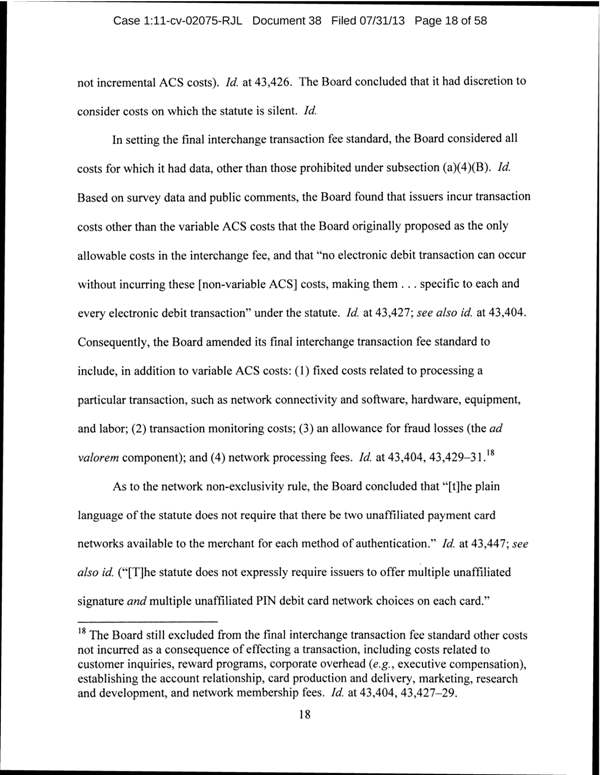

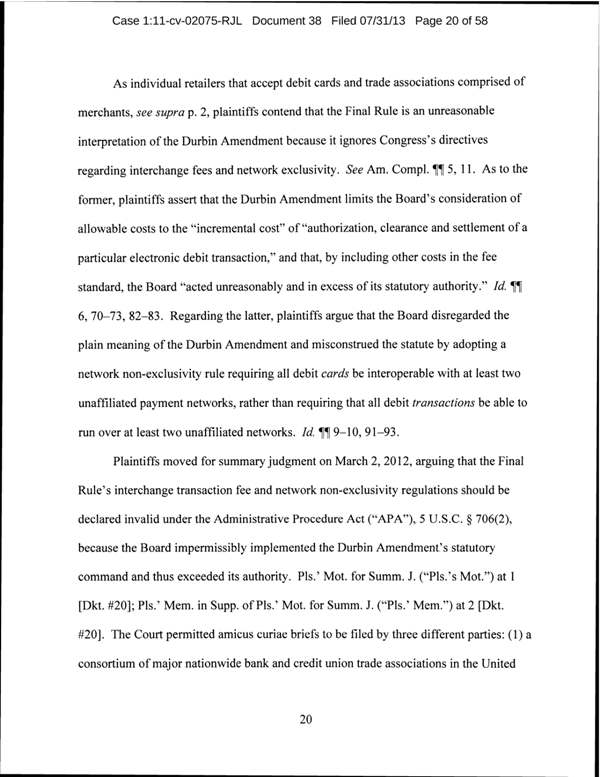

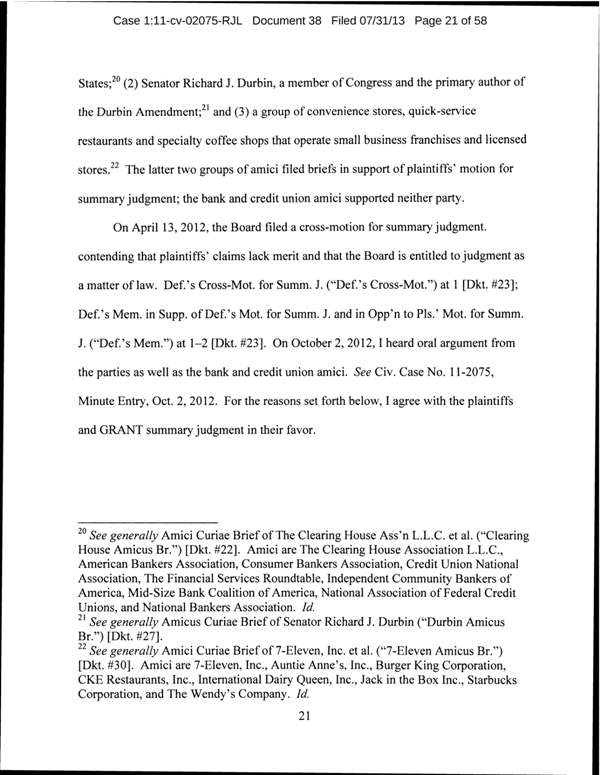

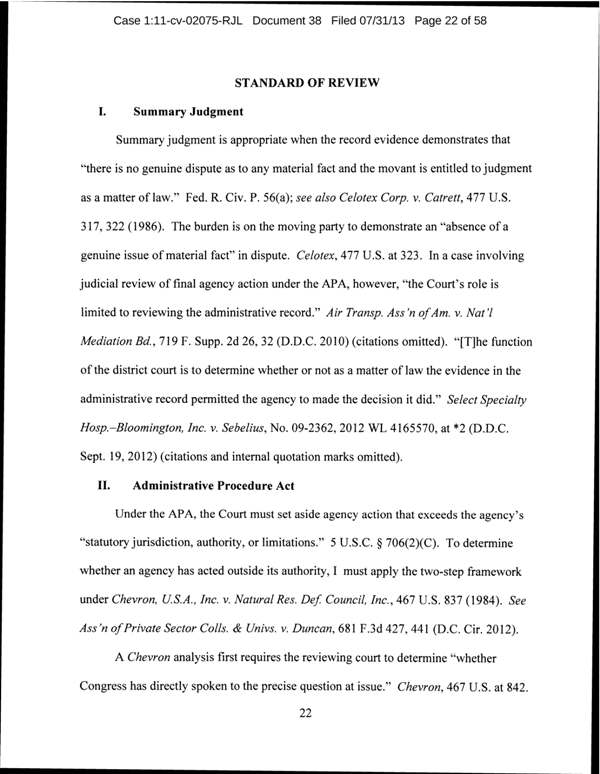

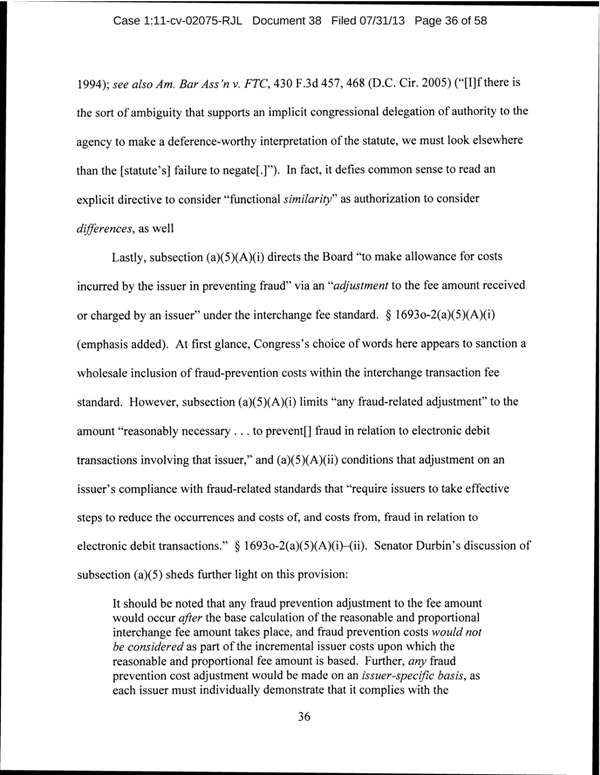

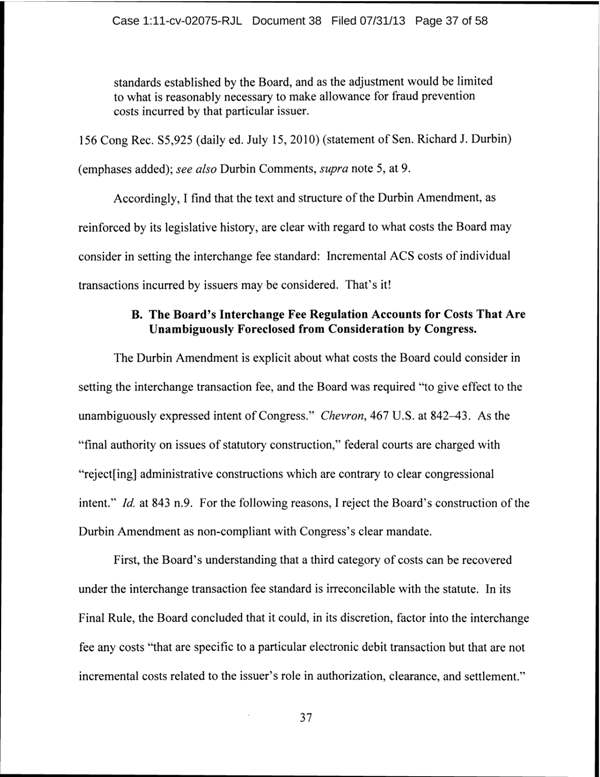

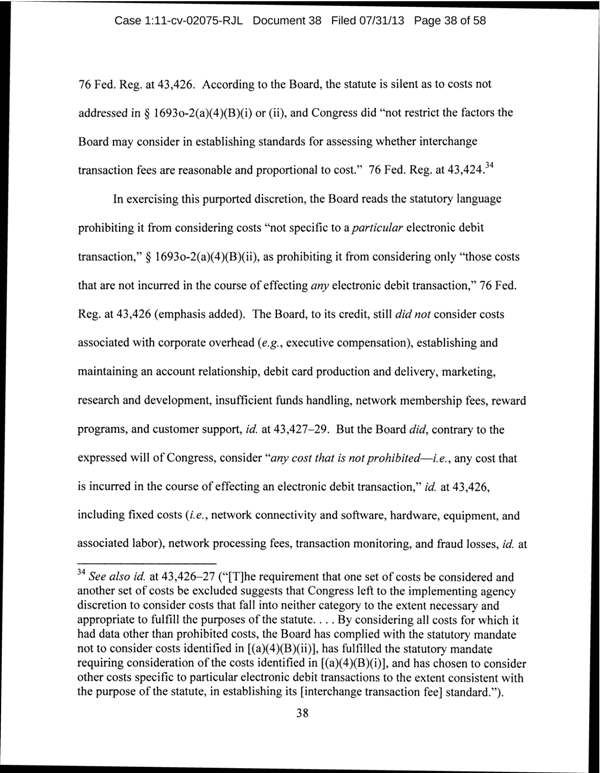

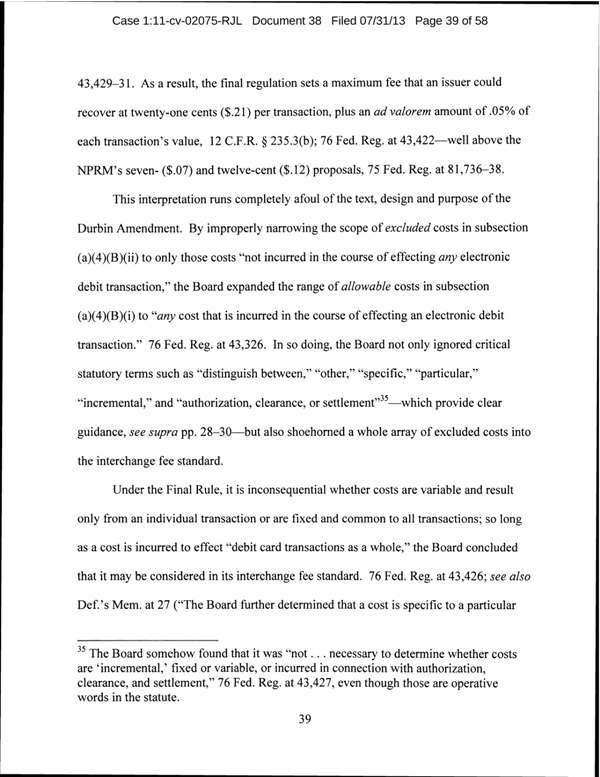

DMR notes from the Federal Reserve Board Order at issue in 11-cv-02075, U.S. District Court, District of Columbia (Washington) that in calculating fees for data processing by entities under Federal Reserve jurisdiction, the new Federal Regulation, 12 CFR Part 235 Federal Reserve Regulation II, “Debit Card Interchange Fees and Routing” the Federal Reserve took into consideration costs that are incurredto effect an electronic debit transaction , including network connectivity costs; costs of hardware, software, and labor used to effect electronic debit transactions; network processing fees; transaction monitoring costs; and fraud losses incurred by issuers. Costs not weighed include corporate overhead (such 1960 as executive compensation, support functions such as legal, human resources, and audit, and the issuer’s branch network); card production and delivery, marketing, and research and development; network membership fees; costs of rewards programs; and customer inquiries. The Federal Reserve capped debit 1965 interchange fees at $0.21 to $0.24 cents- which is comparable to the fee for a stamp on mail in the United States Postal System for much of recent history

DMR puts forth that such a rule is not imaginable for any fee 1970 associated with an industry processing non-financial data in 2011. DMR puts forth that it is possible with the 21st Century Digital Network design to do the same for non-financial data processing on 21st Century Digital Networks comprised of hardware, software, information channel and network admin, such 1975 network enabled by TTS CLAs as described throughout this TTS 7/11 USPTO note by applicant, which elaborates on but does not change any facet of the 12/079,235 patent application.

there are limitations under the bank data processing statutes which effect the goal of efficient data processing on the internet as a whole. The commercial engine effecting Research & Development for secure financial data processing has restrictions in processing trademarks and copyrighted data. Even the banks’ non-financial simple trademarked data- such as customer names and addresses are at risk to fraud continuously. The interchange rate in light of the number of annual transactions (38 billion and growing) in light of the statutory disincentive (discussed below in next paragraph ‘c.’) for the BHCs to process non-financial data contribute to the predictability for one skilled in the art to extrapolate and readily anticipate the effect of a change in the marketplace and regulatory landscape .

c. LIMITATIONS ON APPLYING PROPRIETARY FINANCIAL DATA PROCESSING GOODS, SERVICES, AND TECHNOLOGIES TO NON-FINANCIAL DATA PROCESSING:

Section 4(c)(8) of The Bank Holding Company Act, Title 12: Banks and Banking Part 2035 225—Bank Holding Companies And Change In Bank Control (Regulation Y) § 225.28 List of permissible nonbanking activities, and Title 12 Section 1972 of US Code, the Anti-Tying Restrictions of Section 106 of the Bank Holding Company Act Amendments of 1970 (“Section 106”)

As stated above, there are limitations under bank data processing statutes which affect the goal of efficient data processing on the internet as a whole. For the present purposes of elaborating on Claim 8 in response to USPTO 1/31/11 Office Action, DMR here articulates a sketch of those limitations and their effect on the internet data processing market, and the place of the 21st Century Digital Network solution to the problem which exists. (Please also see DMR’s Application to the Federal Reserve Board and Study on 2050 Permissible Activities for Bank Holding Companies listed in Item 1 of this TTS 7/11 USPTO writing).

Section 4(c)(8) of The Bank Holding Company Act permits a bank holding company to engage, directly or through a subsidiary, in activities that the Board has determined by order or regulation 2065 to be “so closely related to banking or managing or controlling banks as to be a proper incident thereto.” ( 12 U.S.C. § 1843(c)(8)).

Bank Holding Companies are permitted to engage in data processing as per 12 CFR 228.14. The Board’s 1982 Citicorp Order, which effectively enacted 12 CFR 228.14, specifically stated that

“[I]t is appropriate that all reasonable efforts should be taken to assure compliance with the Board’s finding that only the processing and transmission of banking, financial, and economic data is permissible. A limitation on the types of data for which processing and transmission services are offered does not appear excessive, since the technology to 2080 effect such limitation exists.”(68 Fed. Res. Bull. 505 (1982))

That Federal Reserve Board Order regarding Citicorp evolved to Title 12: Banks and Banking Part 225—Bank Holding Companies And 2085 Change In Bank Control (Regulation Y) § 225.28 (b) (14) Data processing.

Section (i)A stipulates that the data to be processed must be financial, banking or economic; and any non financial processing must be limited to 49 percent of the company's total annual revenues derived from data processing. At root FHC (FHC = Federally defined Financial Holding Company, BHC= Federally defined Bank Holding Company) related data processing is an exception to the axiomatic rule that FHCs or BHCs engage only in banking related commercial activities. The exception was borne in 1982, with express limitations which fetter engagement in non-financial data processing for the most developed, resource-rich data processors in the landscape. Further, additional limitations prohibit FHC and BHC endeavor into software and hardware. DMR highlights the phenomenon because there is no doubt that there are regulatory forces tying the hands of financial data processors and limiting their foray into non-financial data processing.

This is a problem which merits consideration of related political-economy, law, culture, technology, and business matters.

Title 12 Section 1972 of US Code, the Anti-Tying Restrictions of Section 106 of the Bank Holding Company Act Amendments of 1970 (“Section 106”) which “prohibits a bank from conditioning the 2110 availability … of one product on a requirement that the customer also obtain another product from the bank” also carries weight in deliberation of this subject. Any solution must keep this and related banking jurisprudence in mind. Exceptions to Title 12 Section 972 weigh heavily in the analysis.

In 2011 a limitation to permit the companies which collect revenues for providing the service of processing upwards of 38 billion secure data transfers a year only to process financial data and to place limitations/disincentives on non-financial data processed by those entities is counterproductive and stymies innovation in network development, and has contributed to the way in which the market for non-financial, data processing has evolved, commented on below. If, by regulation, Bank Holding Companies continue to be permitted to engage in financial data processing as per 12 CFR 228.14, then some mechanism is necessary to permit Bank Holding Companies to engage in competitive processing and transmission of non-financial data. If not, innovation will suffer, extant technologies will go underutilized, value will be lost to owners of Trademarked and Copyrighted materials, and consumers will be underserved.

The Durbin Amendment to the Dodd Frank Act is an important recent development which sheds light on the phenomenon. There are no national consumer driven proprietary networks which analogize to the BHC networks that process data 2135 for $0.22 cents per data transfer for the non-financial analogue to money data. Until banks can function unfettered- or properly placed in the data processing industry, the industry is suffering, with a toll on the economy in general. There is no non-financial data processor at the table. There are non-bank technology driven interests at the table, but no parties at the table in the name of secure non-financial data processing presently.

In the landscape of data processing, financial data processing commands fee based revenues whereas non-financial data generally does not. The economics of Internet Commerce are defined by transactional fees for financial data processing, but advertising revenues for non-financial data processing. The root of this fact is an essential element of any process seeking the goal of competitive, effective, efficient data processing (and associated fees).

The present relationship between bank holding companies and national consumer driven commercial digital data processing has to consider 12 CFR 225.28 and 12 USC 1972. Bank holding company owned digital networks could perform digital network services more efficiently in an environment permitting non-financial data processing using bank holding company owned resources, including IP technologies. There is a return on the Research & Development for sound fraud prevention technologies which is not being realized given regulations.

d. NON-FINANCIAL DATA PROCESSING MARKET REVENUES ARE DOMINATED BY ADVERTISING REVENUES, WHEREAS FINANCIAL DATA PROCESSING REVENUES ARE FEE BASED DUE TO THE PROPRIETARY NATURE OF FINANCIAL DATA PROCESSING NETWORKS, REGULATORY WALL BETWEEN FINANCIAL AND NON-FINANCIAL DATA PROCESSORS, AND NON-PROPRIETARY NATURE OF NON-FINANCIAL DATA PROCESSING

The financial data processing market has developed where proprietary (owned) networks process the financial data, producing revenue for processing data securely (the interchange rate is charged, and systems process the data transfer and operate systems associated with the data transfer, including records utilizing hardware, software, and an information channel- owned to form a proprietary digital network which is processing financial data.

Conversely, the non-financial data processing market, by certain factors inherent to the political economy of the United States in conjunction with the evolution/history of Internet Commerce has developed where propriety networks are anathema, due to the fact that consumers purchase hardware, software, and information channel independently from different vendors. The industries and markets are equally separate and independent by nature. Every economist and most observers are familiar with the “network effect” in certain product markets- whether it has to do with a network or not- sometimes the network effect can make a product more successful than similar products which do not reap the benefits of the network effect. It goes without saying that consumer driven commercial digital “networks” are a type of product where the network product in fact benefits from the “network effect” as compared to the network product which achieves less of any network effect attainable in its market. Here, the network product is a proprietary network comprised of hardware, software, information channel (controlled by information carrier), administered under some management.

In the consumer market for internet technology, consumers purchase hardware, software, and information channel independently from different vendors. There is a limit therefore imposed on the network effect benefits bestowed upon / reaped by 2210 the network product comprised of the combination of those products. (Because banks were permitted to process financial data, their network products comprised of PNCC 1, 2, 3, & 4 evolved in proprietary nature). An analogous evolution in the consumer driven non-financial data processing market of 2215 proprietary combinations of hardware, software, information channel, and network administrator was “anathema” to the self same telecommunications industry, operating system industry, hardware industry in the US marketplace. The applied for innovation is a method to cure this phenomenon, to spur 2220 proprietary networks for consumer driven internet technology related digital commercial networks processing trademarked and copyrighted data.

The Federal Reserve Board Order final rule on debit card interchange fees and routing and interim final rule on fraud prevention adjustment is a case in point to illustrate the present phenomena alluded to in the above paragraphs. The interchange fee is in fact the charge for processing ‘owned data’. The other species of owned data apart from financial data is trademarked or copyrighted data. Owned systems process financial data in 2011, so the Federal Reserve Rule is feasible. Owned systems do not process Trademarked and Copyrighted data in 2011, so such regulation is not even conceived of in 2011. It follows that the costs considered by the Federal Reserve for processing financial data are not being directly collected for the analogous services in the Trademark and Copyrighted data processing industry, contributing to an overall loss of myriad efficiencies in that industry.

21st Century Digital Networks address this phenomenon.

In 2011 United States of America, there is no such large scale processing of data as product for any of the non-financial data processing tasks in popular or desired use with revenues per data processed which revenue in turn supports R & D, Fraud Prevention, and Customer Service or Technical Support for the digital network product which results from a combination of goods and services offered by PNCCs . For there to be such a product on the market (without the current applied for 21st Century Digital Network innovation product), such network product used by consumers would have to be comprised of hardware, software, and information channel- with a managing administrator all under one corporate entity.

Not everyone inthe United States uses AT & T, or Dell, or Microsoft. Conversely, Mastercard or VISA proprietary information channel, hardware, and software networks process financial data charging the interchange rate to merchants to use it. Regulation limits their ability to process trademarked and copyrighted data. Claim 8 indicates how the 21st Century Digital Network system can be used not only to associate proprietary rights for a limited time with networks which process trademarked and copyrighted data to spur development of the industry, but also to permit a mechanism to address the limitations expressed above in this section of TTS 7/11 USPTO and the DMR Articles disclosed in the information disclosure requirement above. FHCs as PNCC Class 4 Network Administrators are particularly well suited because the Federal Reserve has regulated interchange fees and is experienced with its trials and tribulations, and is thereby an appropriate agency to contribute in regulating analogous fees for non-financial data processing. Likewise, the FHCs are appropriate to be Network Administrators for non-financial data processing given experience with financial data processing, including related record keeping, customer service, and importantly the plant and operations devoted to each in place presently. However, in such a scenario, such Networks would have to offer consumers services like recording calls where assurances are being made by Network Administrators, and Notary Services would need be available, and, Network Administrators' attorneys would have to comply with CPLR and Model Code or such Networks would be "unjust". Presently, the behavior of debt collection firms in the litigation at bar is part of an obstacle preventing the evolution of moving companies like American Express from being processors of Financial Data to being Network Administrators, according to Rosenblum. To be certain, in the current environment companies like American Express's policies might also contribute to the stymieing of such evolution- because of the business model which relies heavily on loan interest revenues, and, default judgment revenues, and which ties network services to loans and deposits and discounts. In such analysis, there is also an absurdity that Airline Reward Programs and Rental Car Policies are tied to Credit Card Loans and data processing fees associated therewith.

Perhaps there are other ways to achieve the same. Here, Claim 8 is as to the manner by which the 21st Century Digital mechanism –the TTS CLAs between PNCC Class1, 2, 3, & 4- achieves this task.

Note for example feeding a check to an ATM machine which scans it and deposits the check. Note the bank websites, and the token mechanisms for logging in. None of these mechanisms are in use outside of financial services, albeit the technologies utilized could be easily introduced into non-financial commerce as an enhancement.

If no right were ever given to the process of forging steel, smiths would still be making horseshoes only rather than builders constructing skyscrapers.

Taking the analysis a step further, to advocate one proposed solution for the above problem, without a property right at the level of "internet-technology based network" then the benefits which arise in a market from a property right will not achieve to the combination of PNCCs. Manufacturers of hardware enjoy a right associated with the goods manufactured, as do writers of software, and providers of telecommunications services.. But not one of these markets alone is by itself an internet-technology based network combining all three with an administrator. A 21st Century Digital Network is a species of such network enabled through TTS CLAs between the four PNCCs described throughout. The Patent applied for is the property right linchpin for that market. The industry will only use the 21st Century Digital method if doing so is worthwhile.

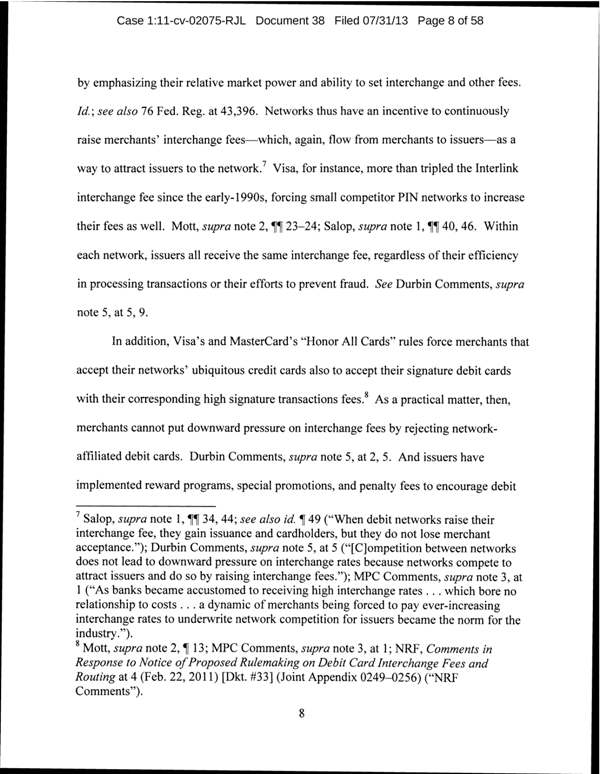

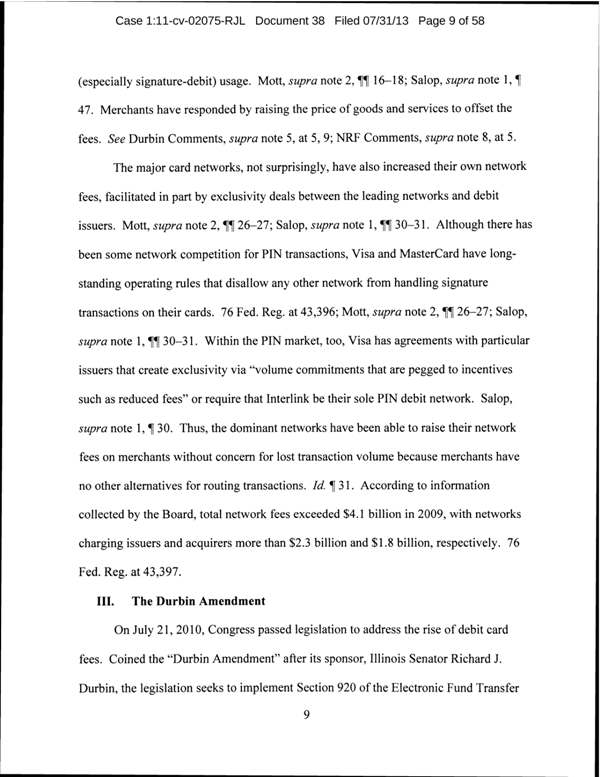

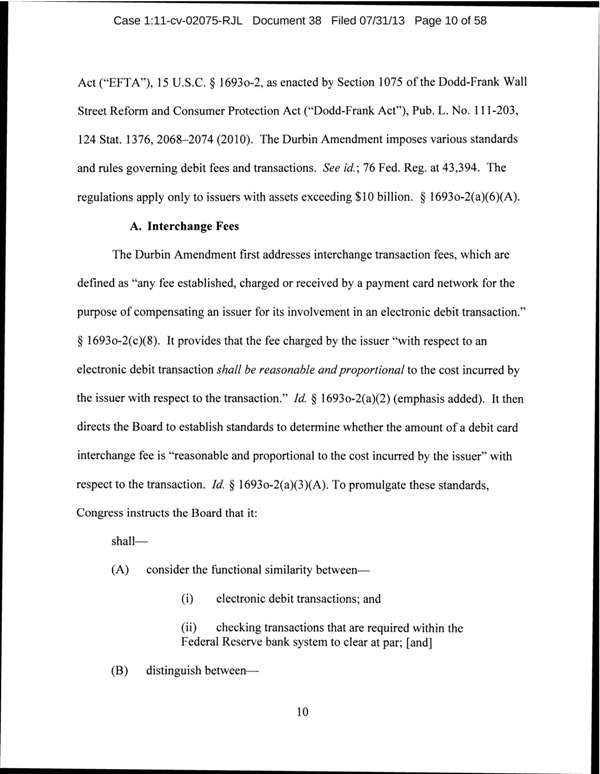

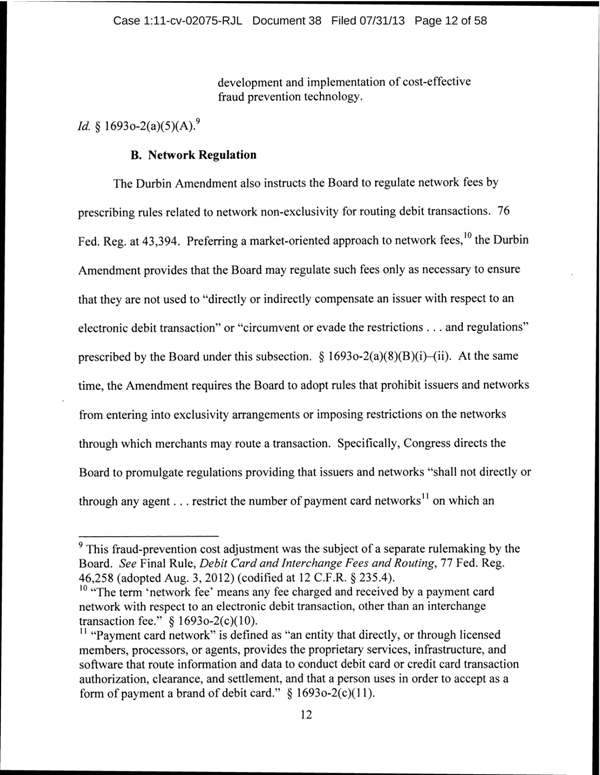

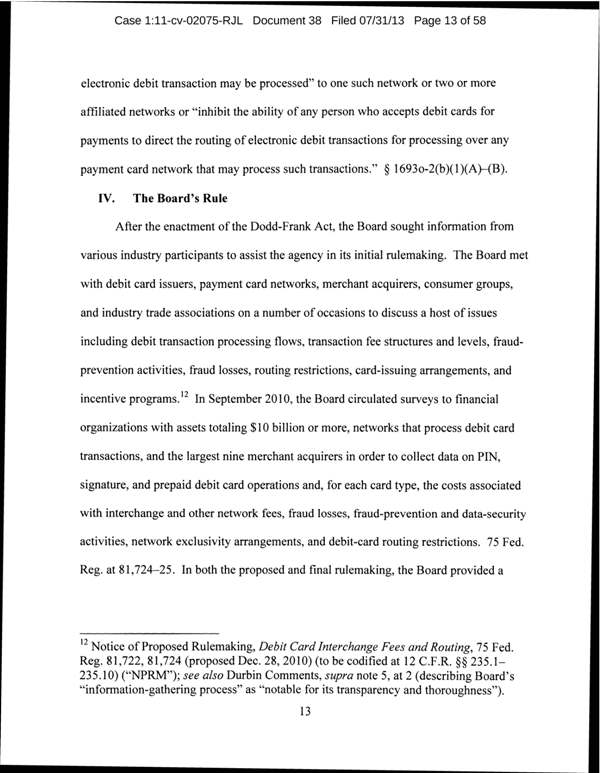

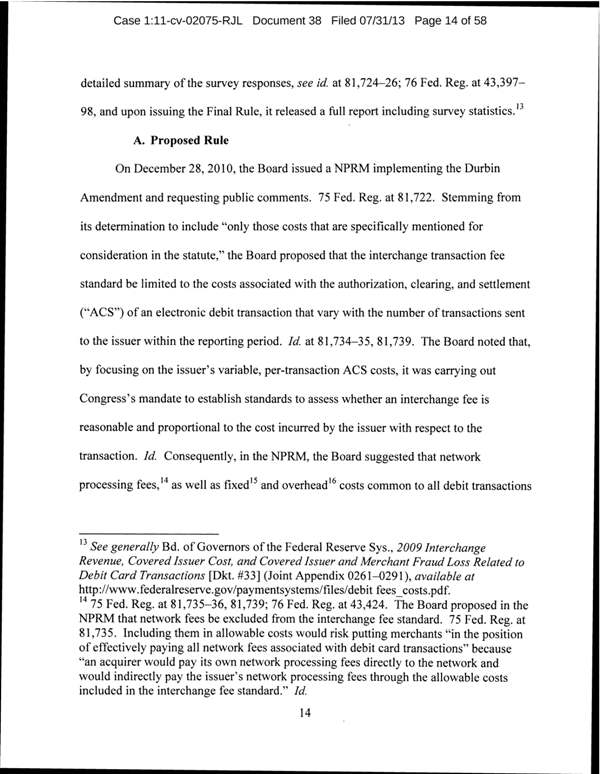

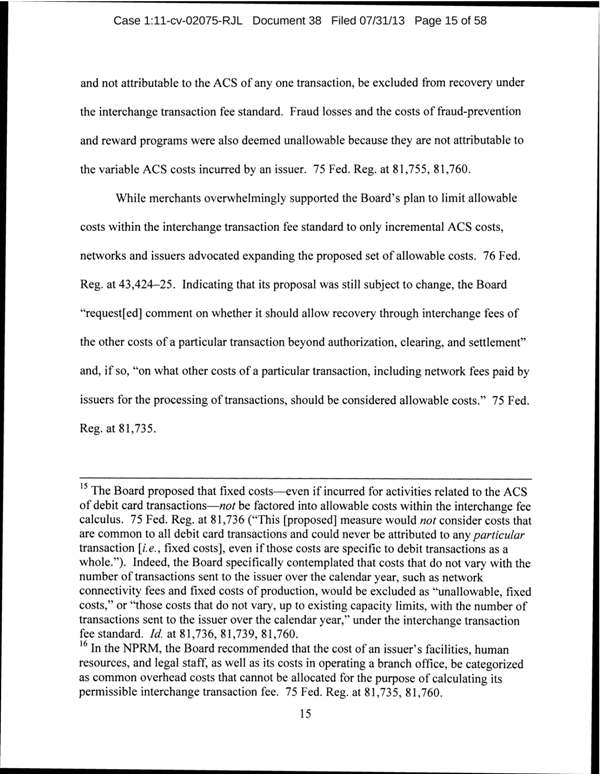

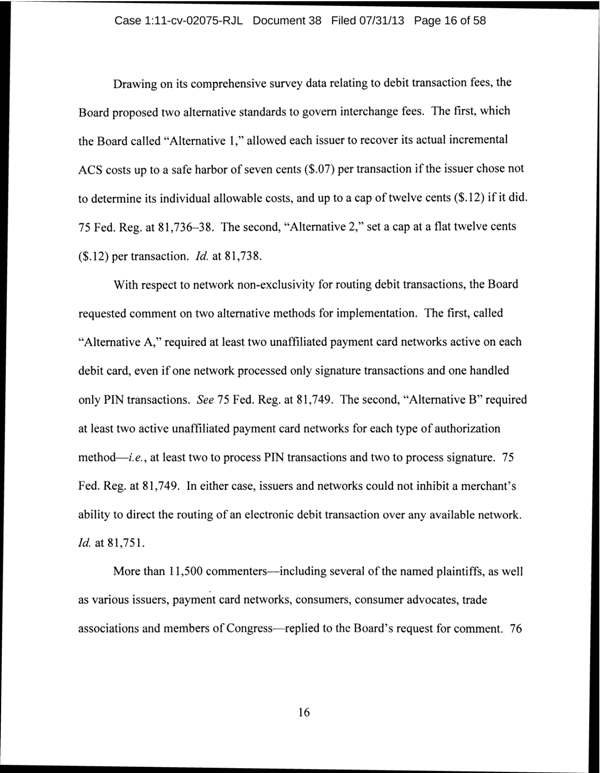

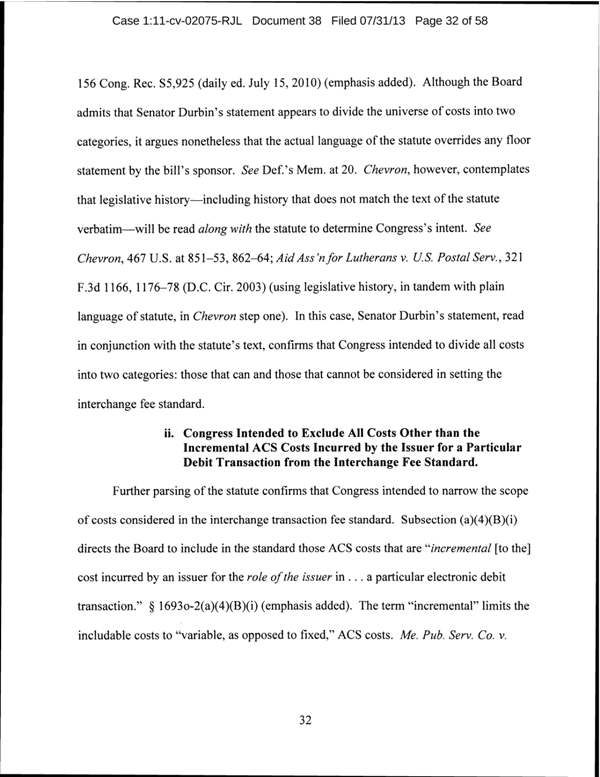

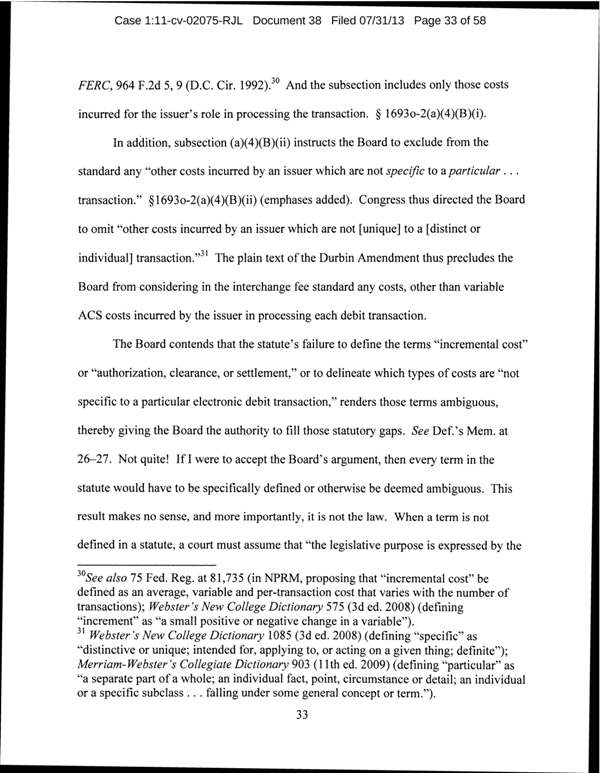

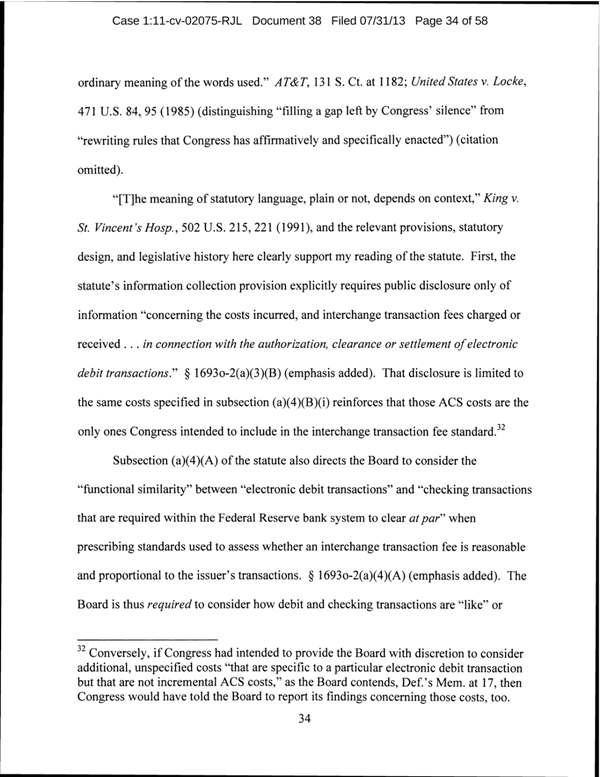

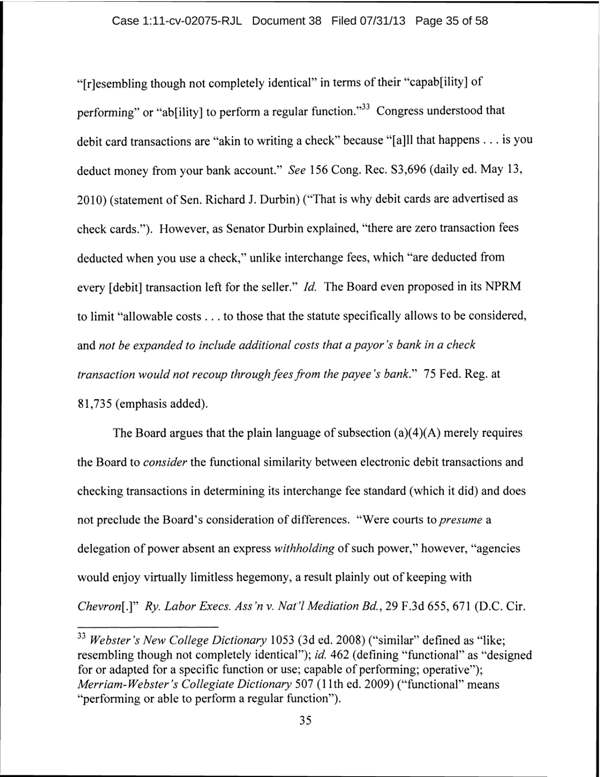

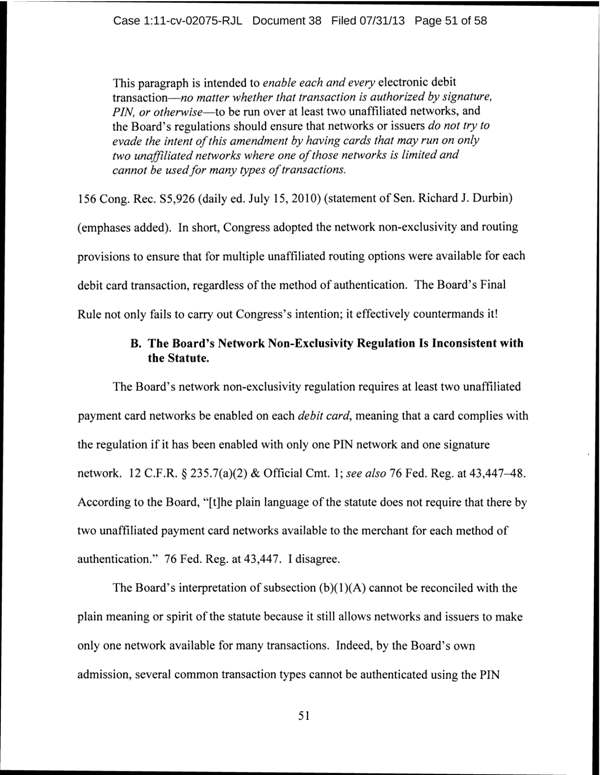

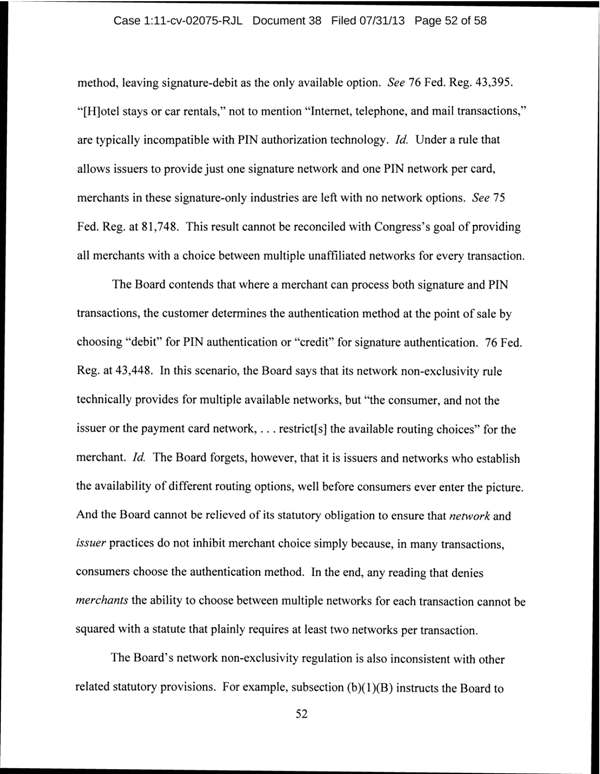

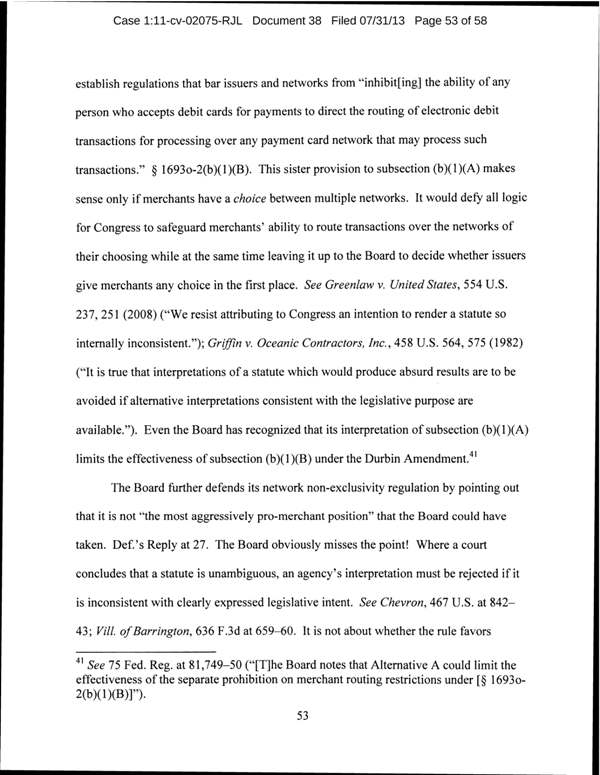

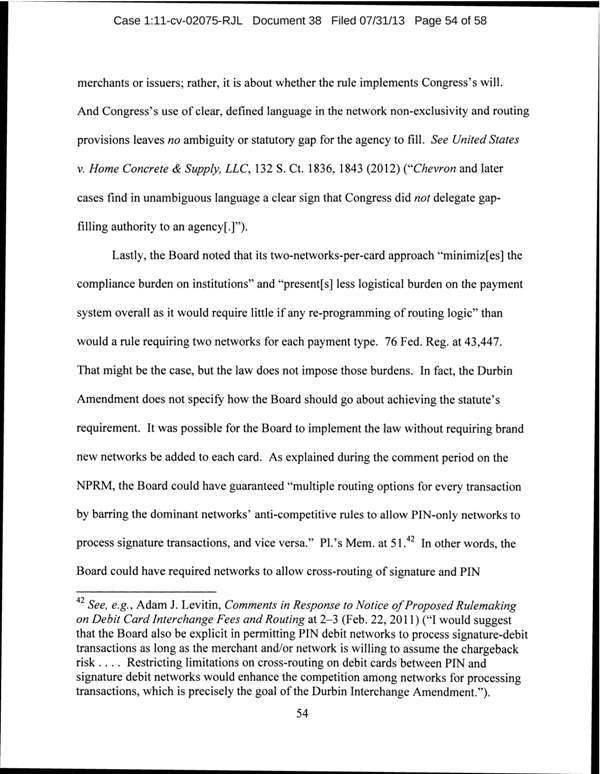

§§¶¶ 40 Images of the full 59 page decision in NACS v. Board of Governors of the Federal Reserve System, 11-cv-02075, U.S. District Court, District of Columbia (Washington)

§§¶¶ 40

Images of the full 59 page decision in NACS v. Board of Governors of the Federal Reserve System, 11-cv-02075, U.S. District Court, District of Columbia (Washington):

<

Affirmed and signed, (certificate of signature in Efile)

Daniel M Rosenblum September 15, 2013